When Growth Becomes the Problem

Most digital lending platforms are built to launch fast, not to last. The early architecture decisions a single database, a monolithic application, tightly coupled services make perfect sense when you're processing a few hundred loans a month. But when volume climbs past 50,000 loans, those same decisions become liabilities.

What follows isn't gradual degradation. It's a sudden, painful wall. Loan approvals slow down. Customers drop off mid-application. Engineering teams spend more time firefighting than building. And the business which was supposed to be scaling starts losing ground instead.

This blog traces that breaking point, explains why it happens, and maps out what it takes to architect a digital lending platform that grows without breaking.

The Real Cost Hidden Behind Slow APIs

Before getting into architecture, it's worth asking: what does a slow lending platform actually cost?

When database locks delay credit checks by even 3–5 seconds, borrowers abandon applications. At scale, this isn't a minor UX issue it's measurable revenue loss. A lender processing 70,000 loans monthly with a 15% abandonment rate due to latency issues isn't just facing a technical problem. They're losing customers to competitors who respond faster.

Regulatory risk compounds this. Manual interventions during audits spike when automated pipelines fail. Compliance overhead that should be systematized becomes a scramble. And the engineering team, instead of building new features, is patching systems that were never designed for this volume.

The technical problems are real. But the business impact delayed approvals, customer churn, compliance exposure is where the urgency actually lives for any fintech lending platform trying to scale responsibly.

Why 50,000 Loans Is the Breaking Point

Early Stage: Monolithic architecture with single database enables fast launch and works well for low loan volume.

Growth Stage: Increasing users and transactions cause heavy queries, performance tuning, and system stress.

Breaking Point (~50K+ loans): High concurrency, database locks, slow APIs, and fragmented data make scaling difficult.

Re-Architecture: Shift to microservices, event-driven pipelines, and cloud-native infrastructure using a structured product engineering approach.

The 50,000-loan threshold isn't arbitrary. It reflects the point at which early design assumptions collapse under real-world load.

In early stages, a single relational database handles everything cleanly. Joins across borrower data, credit history, and loan status run in under 300ms. But as concurrent applications surge, those joins multiply. What once took 300ms now takes 1.5 seconds. API error rates climb past 20%. Memory and CPU hover near 90% during peak hours.

The deeper issue is that initial loan origination system (LOS) was designed around sequential workflows, not parallel processing. KYC checks, AML screening, credit bureau calls each one queued behind the last, each adding latency. Event processing that should run in parallel piles up instead, often exceeding 500ms per request on a system that was benchmarked for a fraction of the load.

Common breaking points at 50,000 loans:

Here is the content in table format (text table for blog use):

| Bottleneck | Impact | Example Metrics |

|---|---|---|

| Database query complexity | Slower joins | 300 ms → 1.5 s average response time |

| API concurrency failures | High error rates | ~20% failure rate at peak load |

| Resource exhaustion | System instability | Memory / CPU usage above 90% |

| Event processing delays | KYC / AML queue buildup | >500 ms per compliance check |

Understanding why this happens is the first step toward rebuilding it correctly.

The Architecture Gap: Monolithic vs. Scalable Systems

Most lending platforms that hit this wall were built on monolithic architectures a single deployable unit where user authentication, loan decisioning, fraud detection, and disbursement logic all live together. This approach works at low volumes. It fails at scale because it can't isolate problems.

When one service degrade say, the fraud detection module gets overwhelmed it doesn't fail quietly. It takes down everything connected to it. There's no fault isolation. There's no independent scaling. There's no ability to update one component without redeploying the entire system.

Modern loan origination system architecture solves this by decomposing the monolith into independently deployable microservices. Each service user authentication, credit scoring, underwriting, disbursement can scale based on its own load, fail without cascading, and be updated without downtime.

Architecture Comparison:

| Aspect | Monolithic Architecture | Microservices Architecture |

|---|---|---|

| Scaling approach | Vertical scaling (bigger servers) | Horizontal scaling (add pods / containers) |

| Fault tolerance | Single failure crashes entire system | Failures isolated to individual services |

| Deployment | Full system redeploy required | Independent per-service deployment |

| Data handling | Shared database with lock contention | Polyglot persistence, service-owned data |

| Peak load handling | Brittle, prone to collapse | Elastic, auto-scales with demand |

The shift isn't just technical. It's a product decision about how the system should behave under pressure and how engineering teams can move faster without breaking what's already working.

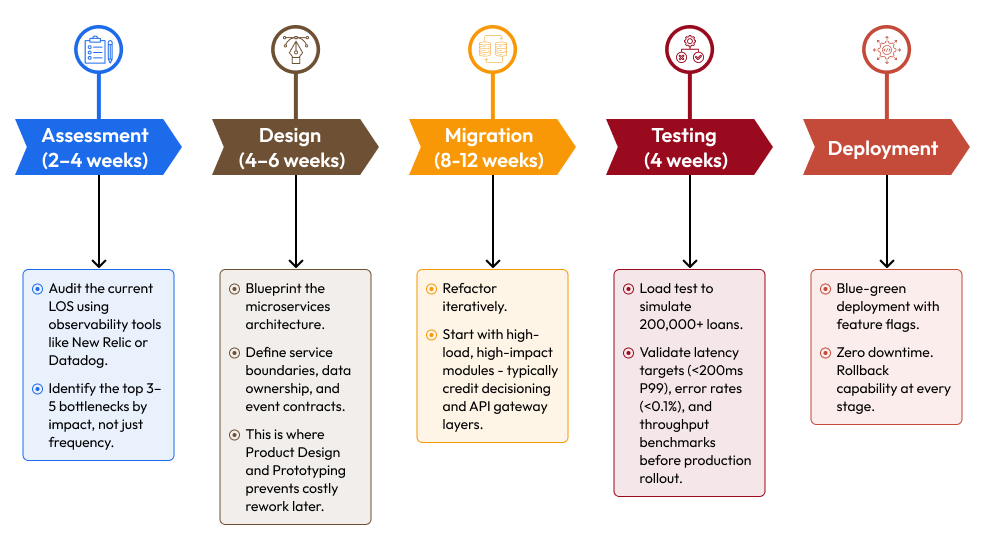

Re-Architecting for Scale: The Strategic Approach

Re-architecture isn't a single event. It's a phased process that requires careful sequencing to avoid disrupting a live, revenue-generating system. The goal is to migrate incrementally, starting with the highest-load modules and preserving stability throughout.

The process typically follows a structured path through Product Strategy & Consulting, then moves into Product Design and Prototyping to validate service boundaries before any code is written each phase building on the last.

The technology stack for this migration typically includes Node.js or Go for microservices, Kafka for event streaming, MongoDB sharded clusters for borrower data, Redis for caching high-frequency queries, and Kubernetes on EKS for orchestration. Serverless Lambda handles burst loads without over-provisioning infrastructure.

The Trade-Offs That Matter Most

One of the most overlooked aspects of re-architecture is the trade-off conversation. Not every component needs to be a microservice. Not every database needs to be replaced. The best lending platform scalability strategies are the ones that apply the right solution to the right problem not the ones that chase architectural purity.

For example, switching to NoSQL for all borrower data sounds appealing, but relational integrity matters for loan ledger records. A hybrid approach NoSQL for profile data, relational for transactional records often outperforms a full migration in both performance and operational cost.

Similarly, event-driven design with Kafka decouples services effectively, but introduces eventual consistency. For a loan origination software development team where loan status accuracy is critical, engineers need to consciously design for this and build compensating mechanisms not discover the gap after go-live.

Key trade-offs to evaluate during re-architecture:

Consistency vs. availability: Which services can tolerate eventual consistency, and which require strict transactional guarantees?

Build vs. integrate: Is a custom credit scoring engine warranted, or does a third-party API serve the need at lower cost and faster time-to-market?

Observability investment: Prometheus + Grafana adds overhead but is non-negotiable at scale. Under-investing here means flying blind during incidents.

Migration speed vs. stability: Moving too fast increases rollback risk; moving too slowly leaves the business exposed to performance degradation longer.

These aren't just engineering decisions. They're product decisions that affect roadmap, team structure, and customer experience. Senior leaders CTOs, Heads of Product need to be in these conversations, not just handed the output.

What Success Looks Like

Fintechs that have completed this transition report consistent, measurable outcomes. Throughput increases 4–5x post-migration. Loan approval latency drops from multi-second averages to sub-200ms P99. Auto-scaling reduces infrastructure costs by 35–40% compared to over-provisioned static environments. And engineering teams shift from reactive firefighting to proactive feature development.

One fintech product engineering team processing 70,000 loans monthly saw API latency spike from 200ms to 2.3 seconds during peak underwriting windows before re-architecting. Post-migration, the same peak periods ran at 180ms with zero incidents during their highest-volume Black Friday campaign.

The business outcome wasn't just technical performance. It was faster approvals, lower abandonment rates, and a compliance posture that could scale with regulatory requirements rather than lag behind them.

KPIs to track post-migration:

Throughput: Loans processed per hour

Latency: P99 under 200ms

Error rate: Below 0.1% at peak

Infrastructure cost per loan processed

Deployment frequency and rollback rate

Future-Proofing the Platform

Re-architecture solves today's scale problem. Future-proofing addresses tomorrow's. For digital lending solutions that want to stay ahead, three areas deserve attention.

AI and dynamic decisioning are increasingly core to competitive lending products not just fraud detection, but dynamic pricing, personalized underwriting, and real-time risk modeling. Integrating ML pipelines via TensorFlow or similar frameworks works best when the underlying architecture is already event-driven and service-oriented.

Blockchain for audit trails is gaining traction for immutable loan record-keeping, particularly in regulated markets where auditability is a compliance requirement, not an option.

Edge computing reduces latency for global user bases by pushing processing closer to the borrower. For scalable lending platform teams expanding internationally, this can be the difference between a competitive product and one that feels slow in key markets.

The Architecture Decision Is a Product Decision

The most important shift for any CTO or Founder reading this isn't technical it's conceptual. How you architect your lending platform isn't just an engineering choice. It's a product decision that determines how fast you can ship, how reliably you can serve customers, and how confidently you can scale into new markets or loan products.

Getting this right requires more than good engineers. It requires a partner who understands both the technical depth and the business context one who can navigate the trade-offs, sequence the migration correctly, and keep the platform stable while the work is happening.

That's exactly what structured product engineering services for fintech are designed to deliver.